Markowitz Portfolio Optimization for Memecoins: Complete Mathematical Guide (2026)

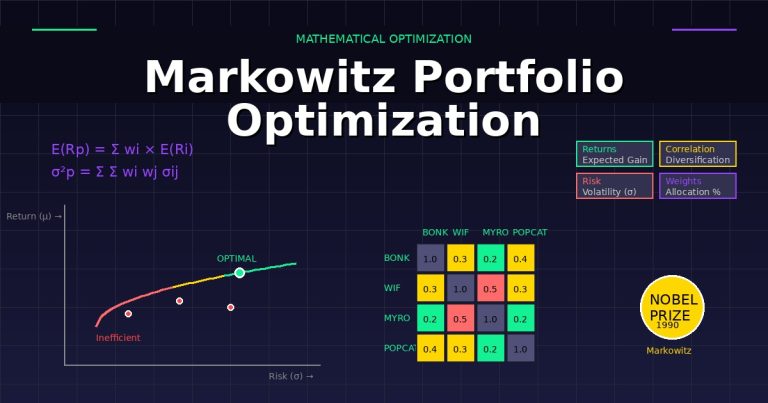

Master Markowitz portfolio optimization for memecoin investing. Complete mathematical guide covering Modern Portfolio Theory fundamentals (expected return, variance, correlation), efficient frontier calculation methodology, covariance matrix construction, Sharpe ratio maximization, and practical implementation for Solana memecoins (BONK, WIF, MYRO, POPCAT). Explains why equal-weight portfolios are mathematically suboptimal, demonstrates correlation analysis importance, provides step-by-step optimization examples with real token data, compares risk-weighted vs equal-weight vs market-cap weighted strategies with performance tables, covers portfolio constraints and rebalancing triggers, and introduces automated optimization tools. Includes mathematical formulas with clear explanations, worked examples showing 25-40% Sharpe ratio improvement, correlation matrices demonstrating diversification benefits, and integration with MemePortfolio.io platform. Nobel Prize-winning framework applied to high-volatility crypto assets requiring specialized risk management approaches.